The Morning Dump today will again be about vehicle affordability, specifically focusing on new data from Edmunds that shows Americans are so underwater on their trade-ins that even James Cameron couldn’t find them.

This is showing up in the failure of subprime lenders, starting with Tricolor Holdings. Did that company crash because of fraud, or was fraud a necessary condition of serving the subprime market?

That’s bleak, so perhaps something a little more positive to round it out? If you wanted a Subaru Outback, but not from Subaru, then Mitsubishi might have the car for you. And if you wanted a GM-built EV in August, but you didn’t want a GM-branded one, you probably got a Honda Prologue.

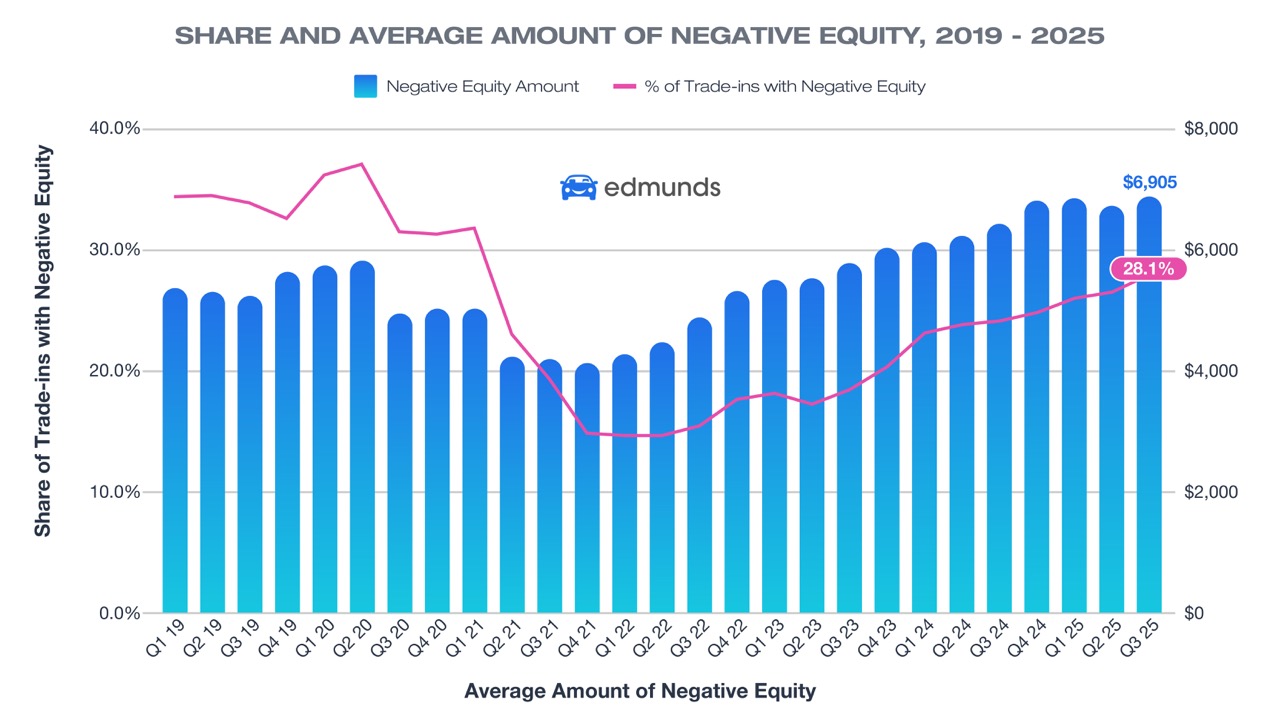

1-in-4 Trade-Ins Carried Negative Equity Of More Than $10,000 In Debt

If yesterday was about how wealthy buyers and electric cars skewed the average transaction price, today’s theme is that underwater buyers at the other end of the spectrum are drowning.

The numbers come via Edmunds, which titles its latest data report “Underwater and Sinking Deeper.” This seems accurate, as Q3 data shows that people trading in cars are extremely upside down on their loans.

About 28.1% of cars traded in last quarter were upside down, with an average amount of $6,905. That’s just the average. About a quarter owed more than $10,000 on their vehicles.

What’s happening? Some of this is the fact that the average trade-in is 3.7 years old, meaning these are the pandemic-era loans I was warning about back in 2023. This is the reaping/sowing moment for those unfortunate buyers. It’s also a sign that people are making even bigger mistakes by trying to buy another car too soon.

“The sheer amount of debt consumers are carrying in their trade-ins should be a wake-up call,” said Ivan Drury, Edmunds’ director of insights. “Nearly one in three upside-down car owners owe between $5,000 and $10,000 — and a growing share owe far more than that. Much of this stems from shoppers trading out of vehicles too quickly, or carrying loans taken out during the pandemic car market frenzy, when prices were at record highs. Those choices are now catching up, making it far harder to buy again without piling on even more debt.”

Americans do not love the idea of downsizing, and it may not always be a reasonable choice for everyone, but it’s probably necessary for many consumers.

“For many car owners, there’s no quick fix for being underwater. It’s about minimizing how much deeper you go,” said Joseph Yoon, Edmunds’ consumer insights analyst. “If you can, wait until you’ve paid down more of your balance before trading in. But if you do need to replace your car, make sure your next purchase fits your budget, not just your needs. The right vehicle choice can prevent a short-term decision from becoming a long-term setback.”

You can imagine a scenario wherein a consumer took out a loan on a vehicle in 2022 for a car that was overpriced. For whatever reason, this consumer now trades in and rolls that debt into a new car, which is now even more underwater. That works so long as people keep staying employed and don’t take any other hits like, say, an increase in healthcare costs due to the expiration of ACA credits.

Of course, if this were happening, there would be warning signs like the failure of subprime lenders.

‘When You See One Cockroach, There Are Probably More’ – Jamie Dimon

JPMorgan & Chase, the New York-based megabank, had to take a $170 million charge-off on the third quarter related to its exposure to Tricolor Holdings, a subprime auto lender.

According to Bloomberg, the quote above comes from JPMorgan boss Jamie Dimon, who added that “Everyone should be forewarned on this one.”

What does that mean? It sounds ominous.

A little background is required here, as Tricolor had both a very specific client profile as well as allegations of shenanigans. The company is said to have focused on people with low or no credit, including undocumented immigrants. That seems like a questionable area to be loaning to right now, given the shakiness of the job market.

There’s probably more to this than merely loaning to people at the lower end of the market. From another Bloomberg report:

Bankrupt subprime auto lender Tricolor Holdings appears to have been a “pervasive fraud” of “extraordinary proportion,” a lawyer helping oversee its liquidation said in court Friday, underscoring the scale of the company’s alleged misconduct even as investigators continue to unravel its finances.

Initial reports “indicate potentially systemic levels of fraud,” according to a presentation made in court by Charles R. Gibbs, who is representing the court-appointed trustee.

While Gibbs didn’t elaborate on the nature of the fraud, a preliminary examination of Tricolor’s records shows that at least 29,000 loans pledged to creditors were tied to vehicles already securing other debts, Bloomberg reported earlier Friday.

This kind of fraud shouldn’t be that easy to pull off, right? Also, what was the exit strategy here? It sounds like it’s being alleged that the company borrowed money multiple times from creditors for the same vehicle.

The subprime market is already a powder keg, so why not toss a few matches in and just see what happens…

There’s Gonna Be A Mitsubishi Outback-Like Thing

Mitsubishi makes reasonably nice cars at a reasonably nice price for, presumably, reasonably nice people. The brand recently added a Trail Edition trim to the Outlander, which Thomas had some opinions about.

Essentially, it’s a decent deal; it just made some of the best features optional. Perhaps the company is going to fix that? From a press release:

MMNA recently debuted a Trail Edition package on Outlander, and this new model will build upon the graphic features on that vehicle by adding off-road-specific bodywork, off-road-focused drive modes and performance upgrades, and unique interior styling with specific materials. This vehicle will take the company’s legendary Super-All Wheel Control (S-AWC) all-wheel drive system3, honed from Mitsubishi Motors’ 12 wins on the legendary Dakar Rally and on the muddy tracks of the World Rally Championship, to the next level, allowing families to explore further beyond where the pavement ends.

More details, including naming, imagery, technical specifications, pricing and on-sale timing will be the subject of future announcements.

So, it’s another Outlander, just more Outback-y maybe?

Honda Really Needs A Cheap EV Here

The tax credit-fueled boom of Q3 had a fun outcome: according to registration data put together by S&P Global Mobility and shared with Automotive News, the third best-selling EV in August was a Honda:

The Honda Prologue was among August’s biggest winners as registrations jumped 81 percent to 9,005 vehicles. The Prologue was the No. 3 most-popular EV for the month after the Tesla Model Y crossover and Model 3 sedan, S&P Global Mobility said.

Registration data serve as a proxy for sales because some EV makers don’t separate U.S. results or report sales by model. Many automakers also don’t report sales monthly.

The Prologue came with incentives of $12,704 per vehicle in August, compared with $5,813 a year earlier, Motor Intelligence said. In contrast, Honda’s gasoline-powered CR-V crossover had $2,016 in August incentives, the data provider said.

Obviously, the Prologue is a GM Ultium vehicle underneath. This goes to show that there are plenty of Honda buyers out there for a Honda EV crossover at the right price (which is much lower than the MSRP). Or is this a sign that people would buy an Equinox EV if it had CarPlay?

What I’m Listening To While Writing TMD

The sad news yesterday was that legendary soul and R&B singer D’Angelo passed away due to complications from pancreatic cancer. I was tempted to do “Untitled (How Does It Feel)” this morning, but I love his cover of Smokey Robinson’s “Cruisin.'” RIP.

The Big Question

What happens next?

Top photo: Edmunds, Dodge

Honda’s HR-V would make a nice EV, though it’s probably not designed to accomodate that. And of course, it wouldn’t be cheap, since it’s a Honda.

I’m not holding my breath for an actual decent $25K EV, but I remain irked that no such thing exists yet.

Your semi-annual reminder that Mitsubishi still apparently sells cars in the US. 🙂

“This kind of fraud shouldn’t be that easy to pull off, right? Also, what was the exit strategy here?”

Party with topshelf hookers and blow while their Washington minions allocate taxpayer funds for a TARP probably.

I said this before and I’ll say it again. The real problem starts when the warranty on the new car doesn’t last as long as the payments will. Something catastrophic happens to the car outside the warranty and the person can’t afford to fix it because all of their money is still going to the payment. And don’t get me started on the used car payments. Slippery slopes people.

“This kind of fraud shouldn’t be that easy to pull off, right?”

Where have you been?

The Prologue is based on a Blazer EV, not the Equinox EV. I get it, all are on the Ultium platform, but the Blazer and Prologue are a larger variant of it and a little bit more upscale with larger motors than the Equinox EV. I think the big reason the Prologue is selling so well is it’s quite a bit cheaper than the Blazer EV and ends up being priced not much more than the Equinox EV, so you end up with more car for less money.

It also is available with Carplay which may drive some of the sales

100%. I shopped both last year. Went with Honda for CarPlay and, well, Honda.

If the OEM is losing money on the sale at the “right price,” it’s not exactly a sustainable business model. This is why the industry is pivoting away from BEVs.

GM is cash flow positive on Ultium so, even with the discounts, they seem to be profiting. Most of the reason why automakers lose money on EVs is because of development costs. That works its way out eventually, as Tesla, GM, and Kia/Hyundai have proven

Yea that’s not true. See below.

https://cleantechnica.com/2025/10/14/gms-ev-production-retreat-leads-to-a-1-6-billion-financial-hit/#:~:text=Of%20note%2C%20GM%20announced%20late,2027%20Bolt%20using%20CATL%20batteries.

But you’re not wrong about development costs being offset eventually… with large scale production. That requires strong demand.

The 1.6 billion was a write off mostly for equipment. That doesn’t factor into being cashflow positive–i.e. they make more money on selling them than it takes to build them

GM’s Electric Vehicles Finally Earned More Than They Cost to Make https://share.google/Vp4mDMuJ8qnVo807p

So the EV business for GM is still in the red… and my point about the business case still stands.

I said *cashflow positive* not in the black entirely. They still lose money because they are still accounting for development costs. That was entirely my point. They make money on each vehicle sold though, so even with the discounts they are likely still bringing in net money by making sales. They need to make more sales to cover the rest of the development costs. You and I are talking about two completely different things

I’ve had exactly one car loan in my life, for 36 months, with a 50% down payment, and I paid off the loan in 12 months. Bought a new Subaru last year, a ‘25 Forester, with cash. Of course my old car, which I also bought with cash, is 22 years old, which I still have (my dirty-job work vehicle) and has crested 300,000 miles. Just installed a new clutch, myself (and not long ago a new starter, radiator, CV shafts, lower A-arms, ball joints, A/C rebuilt – Rock Auto is my friend). That’s a little extreme I admit but if you spoil yourself with a new car every 4-5 years and buy something to keep up with the Jones’s, and you can’t really afford it, and who can these days, then you’re going to be crushed with debt on a depreciating asset. I suspect that some of the people turning in 4 year old cars can afford the debt. The ones who can’t need to learn how to budget their finances.

I owned my last new car for 16 years. The one I have now is fully paid off and is 8 years old. I don’t understand how the average trade-in is 3.7 years old. SMH.

I suspect a decent amount of it is people realizing they will not be able to own a home, so maybe just buy a new car so you like you accomplished something. They likely didn’t accomplish anything good, but they may feel like they did.

Every ~4 years?

With thinking like that, they should probably consider vehicles where the seats recline relatively flat so they can sleep on them. I haven’t had to do that in more than 45 years and that was because I didn’t plan ahead for a hotel on a road trip. I plan ahead better these days.

Doing a fair amount of work in the Los Angeles metroplex, a decade plus ago, I saw a lot of people, mostly guys, driving cars that I could tell they really couldn’t afford and that would make lousy used cars due to the not-done maintenance. A lot of BMWs.

Same. Got my current DD new in Dec ’22. Paid it off last month. Have 7+ years of bumper to bumper warranty left and plan to keep it at least that long.

My wife’s car (2020 model) was purchased used in 2021 for cash and still has a bit of warranty left over.

I love cars and really really like nicer cars. But I’m not willing to put myself under financial strain any way to get them. If I can’t pay cash and have to finance for more than 3 or 4 years to get the payment to a tolerable level, I can’t afford it. I wish more people knew that.

Or put another way, if you’re making $50k a year, a $60k car is not something you can afford. Even a $40k car.

I’ve never owned a Mitsubishi. I might consider one if they stopped doing really weird looking headlights.

As the proud owner of one Mitsubishi I am only going to consider another if we bring back the 3rd generation Delica.

As the proud owner of three Mitsubishi’s (actually had four but traded one in) I will certainly consider what Mitsu is bringing down the pike soon. The Destinator that is coming for overseas markets will be a good choice when they bring it to the USA.

But all of our current Mitsu’s are less than four years old so we aren’t in a hurry.

When you’re in a hole, just stop pooping in the hole. Keep your car until it’s paid off and don’t spend so much the next time.

Matt I agree whole heartily with the sub prime market information and maybe add in a comment about the extension of the period the loans were given. Giving 84 months brings the payments down but you aren’t paying on the actual car for 3-4 years just interest.

I love how JP Morgan profits of the subprime market and now after EVERYONE sees another money loan bubble bursting he comes out acting like he is an expert. He just shills to the media trying to push the market in the best direction for JP Morgan. I fail to see why all the media uses him as an expert.

Perhaps we should consider legislation banning the concept of originating an auto loan that has a principal that is larger than the value of the vehicle being sold.

I saw lenders often require their own appraisal when in the process for a home loan. Sure would be interesting to see the impact of a similar policy for cars.

Mitsubishi needs to bring back the Mirage

I agree. We owned two and still currently have one, a ’24 model.

The entire Voodoo album is superb. The horns, keys and Charlie Hunter’s guitar create a lush sonic texture…like the crushed velvet upholstery.

Cruisin’ is an appropriately Autopian track. R.I.P., D.

So a decades long cultural war on education, intelligence, and expertise leads to a society which is dumb and which makes stupid

financialdecisions?Huh.

It’s not as easy to divide and conquer an *educated* population!

This ^^

““For many car owners, there’s no quick fix for being underwater.”

I disagree. A quick fix is to sell the current expensive vehicle for as much as you can, take part of that money and buy a basic reliable car that has a low TCO… something like a used Prius or a used Mitsubishi Mirage and put the rest of the money against the car loan. And then don’t even think about getting a new vehicle until the debt is paid off.

“What happens next?”

Well.. today is Wednesday… so ‘Thursday’ is what happens next.

No… Underwater means that after you sell it for as much as you can, you still OWE money to the lender.

I know that. The point is that you want to pay as much of the loan as possible with the leftover cash to reduce the amount of interest that needs to be paid.

It’s still a relatively quick/quicker fix than other options.

But it assumes that the existing vehicle is far more expensive than a used Prius or used Mirage.

The car is collateral for the loan. You can’t sell the car until the loan balance is paid, the lender holds the title. Many of these people are underwater because they don’t have the money to pay off that balance.

Well if that’s the case, then I guess the only real option is to hang onto the current vehicle until the loan is paid off.

I’m no expert but if they are rolling over into a new loan does that mean they are still good financially speaking? If so I would say best financial decision is keep it and pay it off. You can’t sell it and still have a loan on an asset you no longer possess see the sub loan part of the dump. And since the rollover would mean higher monthly payments just keeping it is cheaper.

Of course this solution doesn’t work for people that are just broke.

Yeah for people who are broke, their best option is to just hang onto what they have for as long as possible… even after the loan is paid off.

It depends.

Option 1. If the current monthly payment is unaffordable, you can trade the car and bury it in the next loan. Keep this next car until it’s paid off (likely 84 months).

Option 2. If the payment is doable, then keep it until you pay off the loan. Likely less than 84 months. More likely to be around 24 months until the amount equalizes in the most common scenario.

I’m sorry to hear about D’Angelo. I never bought anything he made, but whenever KEXP played him, I was happy he existed, and now he doesn’t. I guess the good thing about a record is that there might be an end to new material, but there’s a lot of new-to-me material to look forward to.

Every.Single.Time an article like this is posted, I comment that if you can’t own the car in 60 months or less, that you’re buying too much car. The proliferation of long term loans inevitably means that far too many people will take out a loan for the payment rather than the actual cost of ownership.

Let me say it one more time. If you can’t own a car outright in half a decade, you’re buying too much car.

DaTs sOCiaLiSm

You’re not only buying too much car, you’re paying too much for it. At some point you’re spending enough on interest and fees that you’re basically renting it.

(And yeah, I get it, you’re young with poor credit and high insurance rates and your new job requires you to drive a nice-looking reliable car, and they’re gonna pay you well next quarter or so and and…)

Giving people 6 years is even a bit much, a few years ago people would be calling someone with a 6 year loan stupid. What progress!

Excuse me 60 months is 5 years the calendar is not on the metric system. JKA as in joking but yeah 22 months not 20 months in a calendar year.

The rule of thumb used to be 3 years lol. Then 5, now 7.

I was taught 36 months as well. I get times have changed but stretching out beyond 60 months is just freakin crazy.

And include the car salesperson and dealership are not your friends and not trying to help you. They will do whatever they can to get you to pay more for a vehicle. Always research the car you are looking at for reliability and price

I purchased my first new vehicle about 3 years ago and as they’re working up the paperwork they finance guy says “You have excellent credit. We could get you in an Outback for the same payment.” It’s absolutely shitty tactics.

To quote Clubber Lang . . .

Prediction? PAIN.

The thing about these folks underwater on their loans is that many of them don’t understand how to get out of it and slightly better terms sound good to them. Had a coworker $10k underwater on a $15k vehicle and she wanted to lease a different vehicle in order to get out from under that loan. She saw the lease deals on a Mach E and thought it was a good way to get out of her 25% APR. She wouldn’t qualify for the deals she saw, of course, but a finance department could probably convince her she was getting a good enough deal if she’d gone in.

It’s the same thing that happens with cash back vs interest rate promotions. People are bad at comparing the interest they’ll pay vs the upfront money, usually overestimating the effect of the interest. Same when they want out from under a loan–they’ll spend more to get out of the interest rate than they save on the lower rate.

Financial illiteracy is rampant and purposeful.

Absolutely. Finance departments, financial literacy education, credit rates and even our convoluted tax system are all designed to ensure that consumers need help if they’re going to navigate it successfully.

Which, of course, means that finance industries rake in the money from the undereducated and the people who know enough to hire help.

two types of people love the uneducated. One is MAGA. Emperor l’Orange even says so!!

Yeah the good old DNC doesn’t take advantage of POC since they failed to keep them down on the plantation

If you are comparing the modern DNC to the Civil War-era or even the Jim Crow Dixiecrats, you have missed A LOT of history!! On the same note, Lincoln must be turning over in his grave non-stop like a rotisserie chicken.

“Mah payments are less”

“She saw the lease deals on a Mach E and thought it was a good way to get out of her 25% APR.”

Clearly she thought wrong… assuming you could even call that ‘thought’.

The real problem with people like that is they also use their vehicle as some sort of status symbol.

So they usually won’t do that they really need to do… which is either stick with their current vehicle until the loan is paid off or sell the current vehicle and replace it with a basic vehicle with a low TCO… like a used Mitsu Mirage or a Prius.

Can do that because if they did, they would “look poor”

Can’t have that… right?

In her case, I don’t even think she was interested in the status symbol, she just couldn’t get it through her head that it would cost her less to pay down her underwater loan as fast as possible instead of starting a new purchase with (hopefully) lower payments and lower interest.

She wasn’t overly bright, anyway, and I don’t think she was getting good advice from family and friends. We tried to set her straight, but she quit her job when she had to rotate to night shift, an arrangement that was clearly explained before she started. So I have no idea where she is now or what she drives.

Unfortunately the not overly bright come from not overly bright families and have not overly bright friends. We tend to hang around with similar people. And finance is a tough subject to understand. Did you know widgets weren’t a real thing?

Also the same deal when buying a house. All that front loaded interest causes you to pay triple the sales price of the house. Of course the only worse decision is renting. I need to move back in with my parents.

I knew it! I knew all these people driving around in 80K+ SUVs and trucks were either deep in debt or had a ton of money. Hahahaha! Maybe don’t spend money you don’t have? Perhaps you didn’t need that yacht on wheels after all! {gasp} Zero sympathy.

Even a decade ago I was talking with my neighbor asking how the people in our community were living so large . . . without missing a beat, he said most people were just treading water and it wouldn’t take but a little ripple to put them under.

90-95% of car buyers need nothing more than a base model Corolla (or in a perfect world a base model Corolla wagon). Come on people – buy the stinkin’ Corolla.

100%. If our household had a Civic Hybrid and a second hand Ford Transit, it would take care of 99% of our transportation needs for the next decade.

My household literally drives a Ford Transit and a Honda HR-V. Who are you and why are you stalking me?

I’m harmless . . . I’ll be out of your life once I have a lock of your hair.

That would work only if people were rational – which we are not! I myself bought a 2008 Corolla for cash after my F-150 was totaled. Was it the smart financial decision? Absolutely. Did I love that car? Absolutely not. I finally sold it and bought a used Nissan Frontier. Did I need it? No. Do I love it? Yes! Was it a smart financial decision? Absolutely not 🙂

With a few unfortunate interruptions, I’ve always driven a used Datsun/Nissan 2WD I4 stick-shift pickup, so count me on Team Frontier. And I’ll bet you had minimal depreciation on that Corolla.

I was a Ford guy for YEARS. My first truck was a 96 Ranger, then went through three F-150s. And now? If my 2015 Frontier ever bites the dust, and Nissan is still around, I’ll absolutely get another one. It’s just a GOOD TRUCK. And yes, I just about made my money back on the Corolla. Damn good car, I just didn’t enjoy driving it!

No money lost and you like what you drive, that sounds like some winning there.

Those Frontiers are deeply underrated.

I always wonder when I read people’s posts about being a brand guy and saying how many vehicles of that brand they have owned usually over an average time line, how good are they if you had to buy so many. Now I am an Isuzu fan I drive a Vehicross since I bought it new in 2002, had an Isuzu Amigo I bought used before that I bought in 1991. So 2 cars in 34 years now that is a reason to be a fan and recommend it. 5 cars in 10 years not so much. IMHO not saying that is what you did.

Honestly, I think it goes back to being irrational about cars. Did I have a reason to be so attached to Ford? Not really. My very first car was an 88 Escort wagon, my first truck the Ranger, and it just kind of took off from there. I just fell in love with Ford. But then it got to be like rooting for a college or a sports team; my identity became wrapped up in it. Which is ludicrous when you think about it… Part of being young and dumb at the time, always wanting an newer model, that kind of thing. Defending Ford even when it made no sense, attacking Chevy just because.

I’ve long since grown out of that, and now just love cars and trucks no matter what. I wanted a nice reliable truck, and my little Frontier fits the bill – I don’t care anymore about needing the blue oval on the grille.

I still have very little love for GM though 😉

One step forward two steps back.

Admittedly we don’t have kids, but I drive a 2014 Sportwagen TDI and my partner drives a 2018 Mazda3 hatch, and we’ve never needed “more” car. We bought them lightly used and had sensible payments for a sensible amount of time. Both are efficient but also fun to drive (VW has some mods), and should last us a long time. The wagon has been big enough for landscaping projects, obviously you’re not hauling loose mulch or a literal ton of rock in it, but I’ve never had to make a second trip to the hardware store due to lack of room.

Also people who decide I can’t afford to pay for an $800 repair job every year on my paid for car so I am going to buy a brand new car with an $800 a month payment.